Executive Summary

Download the full PDF.

The discussion around reforming healthcare tends to focus on progress the industry makes against prescribed numbers—lowering the rate of the uninsured, boosting productivity, and improving metrics around new payment models. While these high-level measurements are important for tracking performance, they distract from the understanding of the true causal mechanism of how industries become more affordable and accessible.

Nearly a decade ago, The Innovator’s Prescription showed how disruption could transform healthcare. Yet unlike other industries, healthcare has been largely immune to the forces of disruptive innovation. Whereas new technologies, new competitors, and new business models have made products and services much more affordable and accessible in fields ranging from media, telecom, finance, and retail, the U.S. healthcare sector keeps getting costlier, and is now by far the world’s most expensive system per capita, about 2X higher than the U.K., Canada, and Australia, with chronic conditions such as diabetes and heart disease now accounting for more than 75% of total spending. At the same time, there has been a widening disparity in the quality of care Americans receive depending on their income and where they live.

Regulatory changes have aimed at shifting costs and risks around the system yet have largely missed the true nature of the problem—the fundamental disconnect between what patients need in order to maximize their health and what they actually get as consumers: more services and treatments that generate revenue. Due to this disconnect, even the shift from fee-for-service to value-based care, while helpful, has not yielded the expected benefit.

While it’s taken longer than expected, we can now point to promising solutions in the marketplace. In Part I, we set the context, focusing on why disruption has not taken hold in the delivery practices of hospitals and physicians groups. In Part II, we zero in on how disruptive solutions have begun to improve health while lowering costs for significant populations.

Those solutions lead to our key recommendations:

- For providers: The business model of extended care teams that include health coaches is driving the ability to deliver holistic primary care tailored for each individual—lowering costs and hospitalization rates. We recommend developing and leveraging new mechanisms for scaling this model.

- For payers: Medicare Advantage has become a successful marketplace that provides the context for disruption. We recommend scaling its cost-saving pilots like the Diabetes Prevention Program that improve health by helping avert or manage chronic conditions.

- For legislators: Instead of shifting rising costs among different stakeholders, focus on enabling models of care that lower costs by maximizing population health. Continue to support the shift to value-based payments and fostering a robust individual insurance market to motivate health plan innovation around consumer needs.

- For all innovators: Understand how urgent imperatives are changing the basis of competition—driving all stakeholders to develop new strategies, business models, and innovation capabilities

EDDIE YARBOROUGH IS 53 YEARS OLD and works in construction near Boston. He went to see his primary care doctor about some joint pain that might be related to recent weight gain. The doctor’s office ordered blood work ahead of time, and during a 10-minute examination, told him that elevated glucose levels signal that Eddie may be on a path toward diabetes. The physician prescribed pills to help regulate Eddie’s blood sugar while also recommending a low-carb diet and regular exercise. On the way out, Eddie agreed at the front desk to set up a check-in appointment for six months.

This kind of interaction is typical of the Traditional Healthcare Delivery System, and on the surface, there is nothing wrong with it. After all, it’s up to Eddie to change his lifestyle, and in the meantime, the doctor and the pharmaceutical company need to get paid by the insurance company for their products and services. But what if it doesn’t work out so well and the patient develops a chronic condition that requires 60% higher annual care costs for the rest of his life?

Too often, that is indeed the case. A physician we interviewed ruefully called this “good luck! medicine,” echoing the frustration many in the profession feel, knowing that this approach is painfully inadequate. At the end of his short visit, Eddie is simply left to wonder just how he’s going to change his behavior given all that is happening in his life—things that the doctor could hardly even begin to discuss given the constrains of the way he practices.

Of 11 Developed Nations rated on their healthcare systems, the U.S. ranked…

As a result of millions of missed opportunities like this, long-term indications for the U.S. healthcare system have grown dire. While the U.S. leads the world in medical research and biotech breakthroughs, it also has the world’s costliest care system, representing nearly 18% of GDP. About a third of $3.2 trillion dollars in annual spending is wasted—lost in paperwork, unnecessary procedures, lack of coordination, and other inefficiencies.That all translates into rising insurance premiums. While the number of uninsured has dropped dramatically in recent years, deductibles and out of pocket consumer spending are on the rise. Chronic conditions ranging from asthma to diabetes to depression to cancer now eat 75% of the total. Despite such spending, the U.S. ranks near the bottom among developed nations in average quality of care, and life expectancy has started to decline for the first time in decades.

High costs and uneven levels of access are typical hallmarks for an industry that is ripe for disruption. The Theory of Disruption states that new entrants start with addressing “non-consumption,” major gaps in the market where certain products and services simply aren’t being purchased or used. By gaining foothold markets, disruptors can move forward with improvements that capture more sophisticated customers and complex markets. Just as Netflix began with DVDs by mail and then moved to online streaming and Amazon started by selling books online and then moved to create an e-book ecosystem, disruptors should be able to transform the health care industry in stages over time.

In healthcare, however, there are forces in place that have made the industry impervious to even the strongest forces of disruption. End users, the patients, have a hard time influencing the design of the end product and often lack control over the buying decision. Health insurance is typically purchased once a year, with the buying decision often being made by an employee benefits manager, or someone other than the end user. New entrants must be invited into the industry by existing incumbents. Provider access to consumers or key partners is therefore dictated by the design of the health plan.

In PART I of this briefing we show precisely why the industry has been largely immune to disruption. But in PART 2 we highlight two markets where disruption is starting to break through and take root. The objective is to extract strategies that that can more broadly be put into play by both incumbent institutions and new entrants, with the aim of harnessing these innovations to revolutionize the entire sector. Our special focus is on transforming the delivery system: the networks of physicians, clinics and hospitals that account for heart of the challenge.

PART 1: Why has healthcare been so resistant to disruption?

For decades industry experts have lambasted the existing fee-for-service model in healthcare. The drawback has been correctly diagnosed: when doctors and hospitals are paid for office visits, procedures, and tests, they will aim to generate more of those, whether or not they are absolutely needed. This not only drives up costs but can actually harm patients. That’s because this focus on transactions often doesn’t directly address the bigger underlying health issues that patients are struggling with in their daily lives.

This profound disconnect between what we need and what we get from the system lies at the root of America’s healthcare crisis.

In the 2008 book, The Innovator’s Prescription, Clay Christensen and colleagues described how disruption was the mechanism that would transform the Traditional Healthcare Delivery System – making it more affordable, accessible and effective.

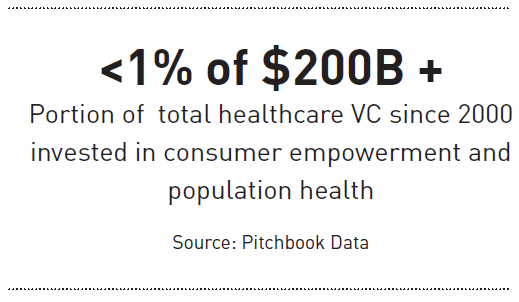

Portion of total healthcare VC since 2000 invested in consumer empowerment and population health.

Yet most of the innovation that has occurred has been sustaining to the industry rather than disruptive. Since 2000, for instance, more than $200 billion has been poured into healthcare venture capital, mostly in biotech, pharma and devices, important treatments that typically make healthcare more sophisticated and expensive. Only a mere fraction of a fraction of 1% of those investments have focused on empowering and engaging consumers to play a more active role in managing their own health. Just 0.65% of these investments have focused on helping payers and providers deploy new technology that enables them to practice population health management.

The Innovator’s Prescription: Reviewing and Updating the Theory

The Innovator’s Prescription: A Disruptive Solution for Health Care

Disruption as we define it isn’t necessarily about startups toppling industry giants but rather a theory about how to make products and services so much more affordable and accessible that they can transform industries and improve the lives of a widening population. To that end, the 2008 book The Innovator’s Prescription explores the role of disruption in tackling the twin scourge of rising costs and uneven quality, offering a solution consisting of three main elements:

- Enabling technology: an invention or innovation that makes a product or service more affordable and accessible to a wider population.

- Innovative business model: a way of targeting non-consumers (those who previously did not buy certain products or services) or low-end consumers (the least profitable customers). This is most easily accomplished by new entrants since they are not locked into existing models.

- Value network: a commercial infrastructure in which partners, distributors, and customers are each better off when disruptive innovation proliferates.

Current value networks in healthcare end up exacerbating the problems of high cost and uneven quality, due to their uncoordinated incentives. But the book describes the operations of a disruptive value network. Kaiser Permanente (KP) is both a payer and provider at the same time. Since it only earns a fixed amount per member, it is driven to utilize resources only when it maximizes the health of that individual. At the same time, it doesn’t compromise quality, and in many cases is able to deliver higher quality and a better patient experience. But KP can do this because its business model grew up that way.

For most providers, the challenge of transforming their business model to deliver better care at lower costs is daunting. The book proposes strategies for deploying new models of integrated care. An integrated system such as KP is organized around the consumer, rather than the service, so that key data, resources, and processes “follows the patient.” It’s analogous to the Toyota Production System that disrupted the auto industry in the 1970s. In Toyota’s case, that meant data flowed with the car through every point in the manufacturing and distribution system, enabling enormous efficiencies.

In the middle of these three enablers needs to be a host of regulatory reforms and new industry standards that facilitate or lubricate interactions among the participants in the new Disruptive Healthcare System. But for reasons that have more to do with industry dynamics rather than regulation, the vision has taken much longer to materialize than previously expected—even though the prescription remains just as valid and promising as it did a decade ago.

Get the future in your inbox.

Supported by incentives in these laws, many industry leaders banded together, shifting from a “fee-for-service” to a “value-based” reimbursement system. The push towards value began long before the ACA, but the law accelerated it. The belief was that by changing the way providers are paid, the industry would have a greater incentive to manage costs and improve affordability of its offerings. The Centers for Medicare and Medicaid Services (CMS) projects that by 2018, over 50% of its payments to providers will be under value-based arrangements. Further, the Healthcare Transformation Task Force, made up of leading providers (such as Advocate, Ascension and Partners Healthcare) as well as major payers (including Aetna, Health Care Services Corp and Blue Cross Blue Shield of Michigan, California, and Massachusetts) has a stated mission of ensuring 75% of payments are made in value-based arrangements by 2020. Many other industry leaders have publicly committed to achieving similar targets for value-based arrangements.

Paying Providers for Value, Not Volume: Percentage of “value-based” reimbursement in Medicare and Medicaid, vs. fee-for-service

Yet changing the payment model alone is insufficient for tackling affordability and population health improvement in a big way. While the shift is still in process, early deployments have shown at best moderate success. For 2014, a total of 97 Accountable Care Organizations nationwide that met the goals of the U.S. Department of Health and Human Services earned bonuses totaling $411 million—about half the savings they produced under the Medicare Shared Savings Program (MSSP). For 2015, there were more than 400 of these partnerships, but total savings only increased to $466 million. While encouraging, that level of savings barely accounts for a tenth of one percent of overall healthcare spending.

Our diagnosis for this underwhelming result: providers are being increasingly paid to deliver value, but if they don’t have the right business models for doing so, their chance of success is quite slim. Healthcare will not become more affordable and accessible by changing just the payment model. Disruption requires an entirely new set of business models that includes fundamentally changing how care is delivered.

After all, the U.S. still pays on average two- to three-times more per procedure than other developed economies. A Kaiser Family Foundation study shows that average family premiums rose 20% from 2011 to 2016. That rate of increase is lower than the prior five years (up 31% from 2006 to 2011) and way below the five years before that (up 63% from 2001 to 2006). While increases in healthcare costs have slowed in recent years, the average cost of healthcare for a U.S. family is still staggeringly high.

After all, the U.S. still pays on average two- to three-times more per procedure than other developed economies. A Kaiser Family Foundation study shows that average family premiums rose 20% from 2011 to 2016. That rate of increase is lower than the prior five years (up 31% from 2006 to 2011) and way below the five years before that (up 63% from 2001 to 2006). While increases in healthcare costs have slowed in recent years, the average cost of healthcare for a U.S. family is still staggeringly high.

The aggregate rise has taken a huge toll. With near stagnant wage growth, the average covered family now spends upwards of 10% of income on health insurance premiums, copays, and deductibles, up from 6.5% a decade ago. This pain is felt most acutely by the lowest-earning individuals and families—squeezing out critical investment in other areas like nutrition and education that foster long-term health and productivity. The wide-ranging effects of the high cost of healthcare will likely only further exacerbate the health (and therefore cost) challenges facing the U.S. for decades to come—unless critical counter-strategies are put in place.

Why more competition in care delivery actually drives costs higher

To understand why healthcare has been so resistant to disruption, we need to examine unique characteristics that drive supply and demand choices.

Competition in healthcare delivery is fierce. In Boston, for instance, leading teaching hospitals are right across from each other, offer the exact same services, and compete for the same payers and patients. This is true in dozens of cities across the country. The economics of supply and demand typically lead to price efficiencies in industries over time: when supply rises or competition increases while demand stays the same, prices fall. But in healthcare, the economics have some special effects not seen in most other sectors.

The Innovator’s Prescription described how more competition in healthcare delivery leads to higher, not lower, costs. This is due to the fact that demand for healthcare services is actually driven by supply – meaning increases in supply lead to increases in demand. A community that adds more hospital beds will see hospitalization rates increase despite no change to the underlying health status of the population, as providers will seek to maximize the use of their assets.

As a result, large systems tend to compete in a way that can be likened to an arms race. Hospitals and care practices choose to add advanced diagnostic gear and build additional capacity to differentiate themselves from other similar local competitors. It’s why you will often see a famous hospital add a new state-of-the art surgical wing named after a large donor. These sustaining innovations signal quality to corporate benefit managers in the hopes of attracting incremental volume. But in order to fund it all, providers remain in a never-ending loop of pursuing efficiencies and raising capital—all in the hopes of stealing market share. Therefore, the very mechanism for increasing revenue is to boost assets.

The core of this challenge isn’t regulatory but requires a deep understanding of the delivery system at hospitals and physicians’ practices. Large providers who compete in the traditional way often house multiple business models under one roof—performing medical research and physician training while also doing diagnostics, routine operations, and practicing intuitive medicine for difficult disease cases. As a result of this comingling, operating a hospital or health system is incredibly complicated, with different revenue and cost models fighting for resources and patients. Further, many health systems partner with independent physician organizations, which have their own models.

This complexity thwarts attempts to calculate key financial and operating metrics like cost and profitability per procedure. It’s difficult to manage costs when you don’t know what they are. That’s why institutions of this size and scope primarily focus on utilization of assets in order to cover what is a predominately fixed cost base. Providers compete by adding resources and capabilities. Then they are under pressure to monetize those assets, so they use them whether necessary or not (we call this “creating demand”).

Healthcare’s arcane fee-for-service reimbursement systems reinforces these behaviors. If costs increase in a given year and additional capacity is also added, it will inevitably lead to higher reimbursement rates next year. This is because providers with a strong brand and significant market share are far better positioned to demand higher reimbursement rates from health insurers. Such providers become close to “indispensable.” When this happens, no competitive insurance offering would consider excluding it from the network. In other words, there is no normal way to resist such leverage. Powerful providers get away with passing higher costs onto payers who then raise premiums.

This helps explain why the move from fee-for-service medicine to value-based care can be so difficult, because it often puts providers in conflict with their own traditional business models.

In order to ease the transition to new payment models, many value-based arrangements are no more than a traditional fee-for-service structure with an additional bonus for achieving certain benchmarks. Most of these benchmarks are for quality and in some cases may also include cost metrics. These types of incentives demonstrate important progress in the long-term battle to transform our system – but they are not a material catalyst to drive the behaviors necessary to make healthcare significantly more affordable.

How the move to fee-for-value presents a financial challenge

Providers who are courageous enough to innovate their business model and break out of the loop of pursuing these sustaining and efficiency innovations are often confronted with a significant financial dilemma.

A value-based model that incents minimizing the utilization of high cost facilities and procedures generally means lower revenue than its fee-for-service counterpart. The decision therefore to move to value-based puts many Chief Financial Officers in a difficult position: accepting longer-term financial incentives in return for deliberately lower revenue immediately, which further stresses profits and potentially increasing credit risk.

The average health system operates on relatively slim margins of about 2% as well as heavy debt loads. While estimates will vary significantly, the move to fee-for-value has resulted in a 2.5% decline in revenue per patient, according to a 2016 study of five health clinics published by the American Journal of Managed Care. To address the decline in revenue, many health systems look for ways to drive volume increases to offset the reduction in procedure-based revenue.

The Greenville Health System in South Carolina is a case in point. The 15,000-employee, non-profit group spans seven campuses and offers everything from walk-in clinics to academic research. Its shift to value-based care and population health management, however, has put it in a financial bind. The good news is that quality metrics are on the rise, as the focus on preventative health is yielding benefits. For instance, in 2016 the system set a goal to reduce LDL cholesterol measures by 3% in its population, yet the reduction actually came in at 8.5%.

The Greenville Health System in South Carolina is a case in point. The 15,000-employee, non-profit group spans seven campuses and offers everything from walk-in clinics to academic research. Its shift to value-based care and population health management, however, has put it in a financial bind. The good news is that quality metrics are on the rise, as the focus on preventative health is yielding benefits. For instance, in 2016 the system set a goal to reduce LDL cholesterol measures by 3% in its population, yet the reduction actually came in at 8.5%.

But to compensate for higher spending as it invests in and offers new care models, Greenville has had to cast a wider net of partnerships and serve more patients. Total outpatient visits, including ER and home health visits, increased from 3 million in 2014 to 3.6 million in 2016. This resulted in higher revenue, growing from $5 billion to $6 billion. But operating income was down dramatically, shrinking from $61 million (1.2% margin) to $23 million (0.3%).

Investing In value-based care follows a typical J-curve model, in which financial performance suffers in the short term.

The squeeze on operating income means there’s less money to invest in new systems— as well as less return for shareholders or other investors. There’s no way to escape it: Attracting more patients while investing in new kinds of services as margins dwindle is initially taxing on an organization, because the payout is often far away (see J-curve). And it’s Often, systems why many systems have developed very slow migration paths over time. will experiment first among their own employee populations. By demonstrating early progress, health systems create data that can then be used to convince other employer groups to sign up for the new offering. The question, then, is why aren’t there more sign ups among the most profitable groups of customers: the Commercial payers who are willing to accept higher rates for better care?

Healthcare’s Catch-22: the lack of market demand for disruption

The price of care for an individual at a hospital depends entirely upon who is paying. Medicare reimbursement rates are generally set at the provider’s cost for delivering that service. Medicaid rates are often 10% to 15% below that. But Commercial patients are priced at a 40% premium over Medicare. This premium – which is vital for overall profitability – drives delivery systems to pursue sustaining innovations in the hope of luring highly profitable members into their system.

Yet at the same time, every employer in the U.S. is reeling from rising healthcare costs. We would therefore expect to see tremendous demand for business model innovation occurring within the Commercial population. Instead, we’ve seen a rise in cost shifting, in the form of passing on higher premiums to workers by way of paycheck debits, copays, and annual deductibles. The average worker now foots about $5,000 of the annual bill, up from $2,700 a decade ago.

Given the desire to manage cost, it’s surprising that more employers aren’t actively seeking out disruptive healthcare offerings. That can partly be explained by the job that employers hire health benefits to solve.

As an employee benefit, health insurance is a solution to the employer’s job to be done of attracting and retaining talent. Depending upon the industry and the company’s specific strategy, benefits managers make decisions about how “rich” a package of benefits they should offer.

While cost is certainly an important consideration, it is not the only factor in benefit design. Central to the decision of the benefit manager is the desire to ensure any new health plan minimizes employee frustration. Commercial health plans typically include very broad networks – meaning they include substantially all hospitals and the vast majority of physicians within a given geography. Benefit managers favor broad networks in order to avoid the number one employee complaint about health benefits – my doctor isn’t in the network.

However, the allure of wide choice is somewhat misleading for consumers. A particular physician being part of a network does not ensure that a consumer can get easy access to that specific doctor. In many markets, leading physicians operate at above full capacity. These practitioners either have closed panels (not accepting new patients) or availability several months into the future. In practice, choice is not really choice.

Such broad networks simply cost more. By spreading patient volume across a wide array of potential providers, employers and their health insurers lack scale to negotiate more favorable rates with a select group of physicians. In contrast, network designs can be customized to concentrate volume towards a select group of providers, either for the primary purpose of lower cost (“narrow network”) or for the dual mandate of lowering cost and improving quality (“high-performing networks”).

The concept of narrow or high-performing networks is not new. Narrow networks were part of the HMO experience in the late 1990s and in part the backlash from this past experience leads benefits managers to look elsewhere for cost-saving techniques.

Narrow, high-performing networks are one promising way to achieve that, yet they’ve barely been offered in the commercial market. In 2016, according to a study by the Kaiser Family Foundation, only 7% of employers that offered health insurance offered employees a narrow network option. Towers Watson had a slightly higher estimate: 13% of large employers offered narrow or high performing networks to their employees. The negative connotations associated with the concept provide further reason for employers to seek other options to control healthcare costs.

However, when the end user is in charge of making purchase decisions, you see very different behavior than when an intermediary selects a set of health plans. In the individual market narrow network designs are abundant, covering about 50% of the patient population in the ACA exchanges, putting them among the most popular options.

Narrow networks help control costs. But they are embraced only by certain types of plans

These different buying behaviors demonstrate the impact of one product being used to solve different jobs to be done. In other words, benefit managers and individual employees have different objectives, and the cost crisis is exposing just how divergent those objectives are.

This results in a Catch-22 situation. In absence of strong demand from benefits managers, providers have been loath to take on the financial risk of creating newer, more disruptive care models. That’s why so many providers are adopting a wait and see approach.

We end up with healthcare system performance that has not materially changed. Overall costs continue to rise, although rate of growth has flattened. Consumer satisfaction rates are not improving. Even though incumbent business models continue to face cost pressures, healthcare spending concerns get crowded out by other key priorities.

Part 2: Where disruptive solutions are taking root

Despite a system that is by and large been hesitant about dramatic change, there are examples where new disruptive care models are demonstrating real promise, signaling that the industry’s resistance to disruption may finally be at a breaking point.

The theory of disruption suggests that change often takes hold in the lower tiers of a market – when targeting customer segments that are well overshot by current offerings, or those segments that aren’t currently consuming given the cost and complexity of existing offerings.

Enter the world of primary care. The tradition of visiting your doctor for an annual checkup is fine, but there are potentially many missed opportunities in between—an area that we call “non-consumption.” If there were a lower-cost alternative to seeing a highly-paid physician, there could be a way to serve consumers more often. The idea would be to evolve the primary care model so it could address these “lower-tier” occasions, even if they don’t generate much revenue.

After all, it’s been proven that investment in primary care pays off. Studies have shown that states and regions with the highest ratios of primary care physicians have better health outcomes, with lower rates of general mortality, infant mortality, and lower rates of premature death from heart disease and stroke. In one study from the U.K., where primary care doctors get special compensation to practice in poorer areas, a 10% boost in the number of family doctors added ten years to average lifespans. In California, when a law required all Medicaid recipients to visit primary care doctors, hospitalization rates declined significantly.

Despite these proven results, primary care is often used as a feeder mechanism to higher cost specialists and large hospitals—rather than the main way to keep people healthy. The experience for the average American underwhelms and is often anything but convenient. To receive seven to ten minutes with a primary care physician, consumers deal with scheduling and other logistical challenges.

Often times the results are less than inspiring. As with the case of Eddie Yarborough, Americans are told to eat healthier, exercise more, take their medications and maybe seek ways to manage stress. Primary care doctors can refer patients to expensive specialists, and to facilities that offer expensive tests, but they often fall short of getting to know their patients’ daily health struggles on a wider basis.

Thus, a significant gap exists in the market for a health advocate to play the role of problem solver for an individual. Everyone has health questions, particularly in today’s environment with an abundance of health information. Am I getting enough sleep? What type of diet should I follow? How do I know if I am making progress? More importantly, many serious long-term health conditions lurk just below the surface. For instance, about 50% of patients who suffer symptoms of depression do not talk to their doctor about it or seek help.

How care teams can disrupt and transform primary care

Recognizing this giant gap in the market, a doctor trained at the Harvard Medical School named Rushika Fernandopulle set out to create a disruptive way to deliver primary care that could break through the barriers we’ve outlined—by deploying “health coaches” to do things that doctors typically don’t and at much lower cost.

The Iora Model: health coaches as part of a care team

Health coaches assume primary responsibility for managing the patient relationship. They are the ones following up with patients and engaging in an on-going dialogue. But they are not clinically trained; instead these individuals are hired for their empathy and demonstrated experience in solving problems for consumers. Fernandopulle’s first health coach was a hire made from a local Home Depot store. The health coaches are part of a care team that includes a doctor, a behavioral health specialist as well as nurses and support staff.

Fernandopulle started testing this new clinical approach while delivering primary care at his clinic in Atlantic City, NJ. Eventually, he and entrepreneur Chris McKown started a new Boston-based company Iora Health, with the express goal of reinventing the delivery of primary care. Iora’s mission is to “restore humanity to healthcare.” This is a classic disruptive model, which typically begins with inferior performance along traditional dimensions—as coaches don’t diagnose or prescribe, so it might seem that coaches aren’t as good as doctors for your primary relationship. Yet the Iora model is superior in different dimensions, such as helping consumers more effectively manage their own health.

Since its founding in 2010, Iora Health, has attracted more than $123 million in venture funding, and it now operates 37 practices in eleven states serving 40,000 patients.21

The model only works on a fee-for-value basis, with capitation as the predominant payment method. The practices are intentionally built to be small – to foster a close-knit community and ensure the extended care team can know the entire panel is being cared for. The care team is different than what you would typically see in a resource-constrained general practitioners office. Iora clinics typically have two to three primary care physicians and eight or ten coaches.

Iora understands what is often paradoxical for would-be disruptors. Disruptors spend more in certain areas than incumbents, with an understanding that these upfront investments will drive significant long-term cost savings.

The health coach becomes the consumer’s advocate. When visiting an Iora clinic, the patient sits with the coach in advance of seeing the physician to establish an agenda of what the patient wants to accomplish. The patient and health coach determine the topics for the visit and take the lead when meeting with the physician to ensure what matters to the patient is covered. Afterwards, the health coach and patient debrief, to ensure the patient has all the information they need to leave the clinic and understand what is expected of them in order to advance along their own health journey.

The health coach becomes the consumer’s advocate. When visiting an Iora clinic, the patient sits with the coach in advance of seeing the physician to establish an agenda of what the patient wants to accomplish. The patient and health coach determine the topics for the visit and take the lead when meeting with the physician to ensure what matters to the patient is covered. Afterwards, the health coach and patient debrief, to ensure the patient has all the information they need to leave the clinic and understand what is expected of them in order to advance along their own health journey.

This significant investment yields tremendous benefits for Iora. Patient satisfaction scores are exceptionally high, with retention rates at most clinics exceeding 95%. Meanwhile, the highest cost resource in the clinic – the primary care physician – is able to focus their time and expertise on only the topics that expressly warrant their attention.

Another unique feature of the Iora model is the morning huddle, when the entire care team invests an hour discussing the health status of the clinic’s population. Because Iora assumes full risk for its patients, the huddle is prioritized around the patients that require the most attention, not just those who are slated for a visit that day.

To that end, Iora has developed a “worry score” methodology where each patient is rated from 1 to 4 based on their overall health status and needs. Patients scoring a 4 require a specific action—such as an outreach from a health coach. If the patient’s outlook turns for the better, they are moved to a lower worry score, a development that is celebrated. There are other team building actives conducted during the huddle – all in an effort to build a strong sense of community.

As one Iora leader told us: when we first engage with a patient, there is the equivalent of lots of deferred maintenance that has not been done, so we end up investing a lot of time and expense helping people to catch up on their health.

As one Iora leader told us: when we first engage with a patient, there is the equivalent of lots of deferred maintenance that has not been done, so we end up investing a lot of time and expense helping people to catch up on their health.

Scaling the model of coordinated care teams

The model has produced impressive results. Across several different populations, ranging from higher-acuity Medicare to the generally health individual market, Iora has been able to consistently produce significant improvements in the health of their populations. Iora points to a study that hospitalizations are 37 percent lower and health care spending 12 percent lower than with a control group using a more conventional health care system.

This is where we pick up the story of Eddie Yarborough, the construction worker in Boston. After an appointment with an Iora doctor, Eddie was assigned a health coach named Kevin who met with Eddie for an hour at the clinic and found that he was not feeling good about himself. As Kevin learned, Eddie had recently been laid off, and he showed signs of depression, which may have been tied up with his overeating and lack of exercise. Eddie rated a worry score of 4, so Kevin began meeting with Eddie every week. They got to talking about career goals, and Kevin mentioned a training program where Eddie could learn to install solar panels, a job category that is rising 25% annually. They talked about Eddie’s diet and kept track of his eating and his walking through a free fitness app. Eddie soon found a new career, started eating better again, and kept up his exercise. By the time he returned to for his doctor’s appointment six months later, he lost 18 pounds and his glucose levels returned to normal. He was no longer on a path to diabetes, and his worry score was lowered to a 2.

The cost model for this kind of whole-person care has proven effective. Studies have shown that for elderly people, home visits reveal that potentially dangerous environments can lead to falls that quickly add up to millions of dollars in hospitalization costs. By studying a patient’s environment, lifestyle, diet and exercise choices, and other behavioral health variables, a coach typically yields many times the investment in cost savings and improved health outcomes. If a coach like Kevin earns a salary of $50,000 and serves 200 patients at any given time, that cost of $250 per patient is tiny compared to the cost of treating, say, diabetes, which adds up to an extra $8,000 annually. So, for a case like Eddie Yarborough, that small investment pays off big.

In the early going, Iora faced difficulty of breaking in to the industry. As noted, the Commercial market is driven by offering premium benefit plans to attract healthy, younger workers, and those people are not typically lured by having a health coach, which is largely an unknown concept. Eventually Iora was able to break through by focusing on select employers. Iora won early contracts with the Carpenters Union in Boston to take care of its sickest and highest-risk employees and partnering with the hotel and casino workers union in Las Vegas to bring down costs for people who have to pay for their own insurance.

Controlling Costs While Improving Care

Iora’s next scaling breakthrough was winning a contract with a major health insurance company, Humana, to focus on the Medicare population, where given the higher acuity of its members, improvements in health status yield more savings. Humana and Iora agreed to set up dozens of new locations starting in 2015. And Iora is not alone in this market: Oak Street, Omada, Docent, ChenMed, WellMed, Mosaic, and Aledade are some of the others that are gaining traction with this disruptive model of whole-person care teams.

How Medicare Advantage is creating a broad context for disruption

Better provider models can only thrive if there is corresponding innovation taking place in the payer marketplace. The good news is that a large and growing insurance segment, Medicare Advantage, is creating the context for innovation that reduces costs while improving health. The model does so through a number of interacting mechanisms, including annual enrollment windows and value-based payments coupled with incentives to invest in the long-term health of members.

Few would expect that a government controlled part of the healthcare market would be where disruption is happening—but that is exactly what is taking place. Medicare, of course, is the country’s largest healthcare payment system, covering 46 million people over the age of 65 as well as 9 million of their dependents under age 22.26 Medicare has enormous power to mandate reimbursement rates. Medicare’s overhead and paperwork costs are much lower too, amounting to about 3% of costs versus about 13% for private insurance.

Total Medicare Advantage Enrollment, by Plan Type, 2007 – 2015 (in millions)

Importantly, there are two types of Medicare that are offered to beneficiaries. Traditional Medicare was established in the 1960s when the Federal Government became responsible for funding and administering the program, under which providers are paid discounted fee-for-service rates for procedures delivered to beneficiaries. Today, nearly half of Medicare payments are value-based and most of the remaining fee-for-service is tied to quality goals.

A second choice began with the Balanced Budget Act of 1997, when the government first added the option of choosing a type of value-based, capitated payments model. That second choice has evolved into Medicare Advantage, where the Federal Government still acts as the funder, but private insurance companies apply to administer and market the program to beneficiaries. So the federal government establishes the rules, and then lets private companies compete against traditional Medicare.

In paying insurers such as Humana, Aetna

Read how Innosight helped Aetna reinvent their approach to healthcare.

Medicare Advantage plans are clearly addressing the needs of a material segment of consumers, as enrollment in such plans grew from 5.6 million people in 2005 to about 17 million in 2015.28 A closer look at critical success factors of the Medicare Advantage market explains why it is emerging as such an important area for business model innovation in healthcare:

The Medicare Advantage payment model serves as a powerful incentive to focus on innovating to manage cost and improve the health of members. Specifically, it drives both payers and providers to seek ways to minimize costly health episodes and ensure care is coordinated. Insurers are more likely to fund home visits and utilize physician extenders– such as Nurse Practitioners–to enable early interventions for at-risk beneficiaries.

More importantly, capitation drives a focus on holistic care rather than isolated health issues. There is growing research demonstrating the importance of interdisciplinary care teams and their ability to drive quality improvements and cost savings such as significantly fewer hospital admissions.29 By integrating behavioral health and chronic care management, providers are able to drive higher rates of medication adherence and corresponding improvements in health status and cost.

The Advantage system uses Risk Adjustment, as a way to ensure payers are being properly compensated for managing risker populations. Risk Adjustment payments account for differences in the cost of a beneficiary considering demographic and health status differences.

Coupled with capitation, Risk Adjustment creates a powerful incentive to focus on prevention and engaging members in improving their health. When a company like Humana enrolls a new patient, it sometimes gets a financial bonus to serve as an incentive to take on high-risk factors. Therefore, Humana immediately goes to work trying to reduce their risk.

So Humana might send an employee or another contractor into a member’s home to recommend changes: Rip up old carpets that contain microbes. Put in ramps to reduce the chance of falling down stairs. They’ll pay for nutrition counseling and help assure that the patient takes her medications as prescribed. They’ll recommend spending more time with friends and loved ones, which carries real health benefits.

Medicare Advantage is a vibrant Direct-to-Consumer segment. While there are group Medicare Advantage plans offered by employers, the vast majority of growth in the category is driven by the Individual segment, where health plans market directly to consumers to encourage them to sign up for their offerings. By eliminating intermediaries, consumers can select the right plan design that meets their specific health needs. If required, seniors can also purchase additional insurance on top of Medicare Advantage to ensure their long-term health needs are satisfied.

This direct-to-beneficiary relationship creates substantial opportunities for payers to better understand their end consumers – and to customize care plans and approaches to meet their exacting needs. This level of customization is essential for creating greater consumer engagement in their own health – by encouraging consumers to adopt new behaviors that reduce long-term risks and costs to the system.

Unhappy Consumers Can Switch Plans Every Year. Open enrollment in the Individual segment of Medicare Advantage occurs annually. If a member is not satisfied with their experience with either their health plan or doctor, they can switch the following year. Seniors have multiple options, including opting to go back to traditional Medicare fee-for-service. This dynamic ensures that health plans focus on creating value for their members in the current year to retain them for the longer term.

The costs associated with acquiring a new member are significant, so health plans in Medicare Advantage have a strong incentive to hold onto membership acquired in prior years—by investing in activities than improve their long-term health. This leads to a much longer duration relationship than what would typically be seen in the Commercial segment. It would not be uncommon for a Medicare Advantage member to remain with their health plan for nine to ten years as compared to the average Commercial member who remains with a given plan for less than three years.

Since product standards are set by CMS, payers focus on delivering a better member experience. Medicare Advantage payers certainly have flexibility around ancillary benefits – like vision and dental and certain out-of-pocket costs – but compared to other segments (ACA Exchange population excluded), Medicare Advantage players have limited ability to differentiate based on benefit design. As a result, Medicare Advantage payers compete more aggressively on the quality of the experience. These consumer-centric models seek to establish a meaningful relationship with members.

For example, Humana operates physical retail locations where members can come in and have questions answered. Seniors bring up any barrier to better health they’ve experienced and receive personal attention. This focus on providing the time and energy to establish holistic care relationships is borne out in satisfaction and trust ratings. A 2015 JD Power survey showed that Medicare Advantage members scored the program at 774 on a 1,000 point scale, significantly higher than the 679 satisfaction rating among commercial health plans. In 2016, that score increased to 790, with Kaiser Permanente’s version of the program receiving a score of 851.

Cost per patient the Diabetes Prevention Program (DPP) has saved Medicare over 15 months: $2,650.

This big, satisfied patient pool encourages largescale experimentation and innovation. For instance, a pilot called the Diabetes Prevention Program (DPP) has saved Medicare an estimated $2,650 per beneficiary over a 15-month period, which not only covered program costs but helped participants lose an average of 5 percent of their body weight, significantly reducing their risk of developing diabetes. The program is delivered through both traditional primary care groups and hospitals as well as alternative settings such as telehealth networks and YMCAs.

Indeed, the YMCA pilot was shown to save more than $1,100 annually per patient. The core benefit is a series of weekly, hour-long “maintenance sessions” with members of a care team that includes the primary care doctor, a behavioral health care manager, and a psychiatric consultant. The aim is meeting guidelines for diet changes, weight loss, and exercise. Providers get paid higher rates for meeting population health goals. As such, it has some of the same aims as the Iora program serving Eddie Yarborough, who is not yet old enough to qualify for Medicare.

A “Dual Transformation” approach to the Disruptive Healthcare System

The big question for incumbent care organizations is how to go about implementing the changes that have proven to lead to lower costs and consistently better outcomes.

Under “dual transformation,” the core (A) is managed separately from new growth (B) and linked by common capabilities (C)

Thus far, large providers have been resistant to change precisely because their existing practices and business models often conflict with the new models of the Disruptive Healthcare Delivery System. For a more sustainable approach to change, we recommend a model detailed in the new book from Innosight, Dual Transformation: How to Reposition Today’s Business While Creating the Future.

The central insight is that major transformations aren’t single monolithic efforts but rather two distinct and separate journeys. “Transformation A” is about repositioning to the core business to adapt over time to changes in the marketplace, even if those changes result in lower revenue. “Transformation B” is about creating a separately governed business venture that is in pursuit of more disruptive solutions. The aim is to make today’s business more resilient while at the same time creating tomorrow’s new growth engine.

The key is to be selective about leveraging difficult-to-replicate assets and capabilities, such as your brand, your partner relationships, and certain facilities and talent while also keeping the two organizations separate. We call this the Capabilities Link. This “flips” the problem of the Innovator’s Dilemma, in which a successful organization has the incentive to perpetuate itself by seeking the highest profit customers through higher profit products. Instead, the A organization can pursue whatever is best for the patient, under a health-centric model.

At the same time, the B organization can seek out new customers or new services that may be outside the realm of traditional care. That new growth can compensate for revenue declines in A.

For example, Americans spend more than $30 billion on out-of-pocket complementary health approaches, ranging from self-help courses to acupuncture. Americans spent an additional $16 billion on yoga classes and related products in 2016, up from $10 billion four years ago.

Often, transformation means creating entirely new capabilities. For a Disruptive Healthcare Delivery System, it means data needs to efficiently and securely flow from location to location, stretching from a central hospital hub to all the spokes in surrounding communities, from walk-in clinics to digital technology to exercise locations that touch patients in their daily lives. This way, each clinician is equipped with the information needed to deliver high quality, low-cost care at any moment, to any member, at any location.

That requires significant system intelligence. For instance, it’s essential to contain patient leakage—meaning a patient accessing services at a provider not affiliated with the integrated system. In the traditional model, patient leakage is lost revenue, and while frustrating this is not as impactful as it is for a value-based system.

Executing on new health-centric models requires investment in new Resources and Processes. New technology is required to coordinate activities, interact and collaborate with patients. The development of such processes can be challenging. New rules need to be written to describe how integrated teams will deliver care.

Lastly, these models are reliant upon the consumer playing a more active and engaged role in managing their health. Providers have to develop deeper capabilities to understand what drives consumer behavior and how to help consumers adopt new behaviors that reduce the chances of chronic disease. Many of these new processes challenge longheld approaches within the delivery system. That’s why we recommend creating a new organization to develop these new business models.

Recommendations for the future

Despite the regulatory uncertainty surrounding health care, the examples and evidence we’ve shared provide strong reason to believe that creating the Disruptive Healthcare Delivery System is within reach.

While many incumbent organizations have struggled with change, the levels of innovation in primary care and Medicare Advantage provide reason for optimism. These are the sectors where new business models are being created, new capabilities around understanding the consumer are being put to the test, and where a holistic approach to managing long-term health is yielding promising results.

While many incumbent organizations have struggled with change, the levels of innovation in primary care and Medicare Advantage provide reason for optimism. These are the sectors where new business models are being created, new capabilities around understanding the consumer are being put to the test, and where a holistic approach to managing long-term health is yielding promising results.

That is why we believe disruption can accelerate and help meet the twin goals of lowering costs and improving health. Both incumbent care providers and new entrants have developed encouraging business models that are centered around keeping people well and improving the status of health for significant populations. Perfecting that causal mechanism—understanding how to help an individual be as healthy as they can be—is the key to triggering industry disruption. We recommend that provider models such as Iora Health should be replicated and payer models such as Medicare Advantage should be embraced by more providers to serve larger populations. Instead of focusing only on high-level metrics, or introducing isolated change tactics such as new technologies or financial incentives, these models take a much more fundamental approach to the basic way consumers interact with the care system.

Taken together, new models of care coupled with payer models that incentivize their success can form the basis of the Disruptive Healthcare Delivery System. This new system would dramatically bring down costs by focusing care teams and consumers themselves around addressing the root causes of poor health tied to chronic conditions.

The implications are far-reaching, as this new system changes the basis of competition in the economy’s largest sector, leading to new growth opportunities outside the scope of traditional healthcare delivery.

But capturing those opportunities requires new business strategies and organizational structures—as well as tools for designing chronic disease prevention and management solutions that consumers can readily pull into their lives. We will explore these topics in depth in the final two briefings in this series.

Once again, these are our key recommendations:

- For providers: The business model of extended care teams that include health coaches is driving the ability to deliver holistic primary care tailored for each individual— lowering costs and hospitalization rates. We recommend developing and leveraging new mechanisms for scaling this model.

- For payers: Medicare Advantage has become a successful marketplace that provides the context for disruption. We recommend scaling its cost-saving pilots like the Diabetes Prevention Program that improve health by helping avert or manage chronic conditions.

- For legislators: Instead of shifting rising costs among different stakeholders, focus on enabling models of care that lower costs by maximizing population health. Continue to support the shift to value-based payments and fostering a robust individual insurance market to motivate health plan innovation around consumer needs.

- For innovators: Understand how urgent imperatives are changing the basis of competition—driving all stakeholders to develop new strategies, business models, and innovation capabilities.

WATCH INNOSIGHT’S ANDY WALDECK ON CHANGING THE BASIS OF COMPETITION IN HEALTHCARE

ABOUT THE AUTHORS

Clayton Christensen is the Kim B. Clark professor of Business Administration at the Harvard Business school and co-founder of Innosight.

Clayton Christensen is the Kim B. Clark professor of Business Administration at the Harvard Business school and co-founder of Innosight.

Andy Waldeck is a senior partner at the growth strategy consulting firm Innosight, where he leads the firm’s healthcare practice.

Andy Waldeck is a senior partner at the growth strategy consulting firm Innosight, where he leads the firm’s healthcare practice.

Rebecca Fogg is the senior research fellow in healthcare at the Clayton Christensen Institute, a nonprofit, nonpartisan think tank dedicated to improving the world through disruptive innovation.

Rebecca Fogg is the senior research fellow in healthcare at the Clayton Christensen Institute, a nonprofit, nonpartisan think tank dedicated to improving the world through disruptive innovation.

Special thanks to Evan I. Schwartz of Innosight for the preparation of this report, and to Ryan Marling of the Christensen Institute for additional research

ABOUT INNOSIGHT

The strategy and innovation practice of global professional services firm Huron, Innosight helps organizations design and create the future, instead of being disrupted by it. The leading authority on disruptive innovation and strategic transformation, the firm collaborates with clients across a range of industries to identify new growth opportunities, build new ventures and capabilities, and accelerate organizational change. Visit us at www.innosight.com.

ABOUT THE CHRISTENSEN INSTITUTE

The Clayton Christensen Institute for Disruptive Innovation (https://www.christenseninstitute.org) is a nonprofit, nonpartisan research organization dedicated to improving the world through disruptive innovation. Founded on the theories of Harvard professor Clayton M. Christensen, the Institute offers a unique framework for addressing complex social issues like education, healthcare, and global development.